Key Takeaways

- The US housing finance regulator wants Fannie Mae and Freddie Mac to draft plans that treat crypto as part of a borrower’s assets for mortgage review.

- Crypto holdings can be counted directly in mortgage underwriting if the proposals are approved.

Share this article

The US Federal Housing Finance Agency (FHFA) has directed mortgage giants Fannie Mae and Freddie Mac to develop and submit proposals that would allow crypto assets to be included in mortgage underwriting without a mandatory USD conversion.

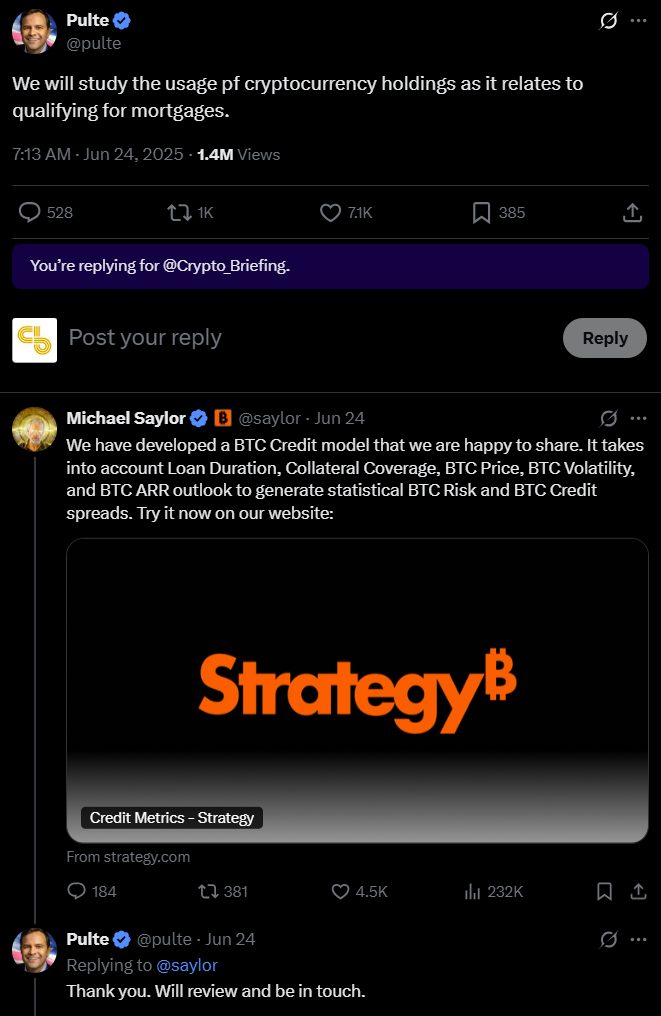

The directive, signed on June 25 by William Pulte, the Director of the FHFA, came shortly after Pulte said Monday that the housing finance regulator would explore the possibility of including crypto as part of the asset evaluation in mortgage qualifications.

Strategy’s Executive Chairman, Michael Saylor, offered to share the company’s BTC credit model, which was created to evaluate creditworthiness based on Bitcoin assets, which addresses loan duration, collateral, Bitcoin price fluctuations, and risk projections, with Pulte.

In response, Pulte said he would review Strategy’s model.

Under the new order, government-sponsored enterprises must consider only crypto assets that can be verified and held on US-regulated centralized exchanges operating within appropriate legal frameworks.

The order also requires both enterprises to incorporate risk mitigation measures, including adjustments for market volatility and appropriate risk-based modifications to the portion of reserves held in crypto assets.

Any proposed changes must receive approval from each enterprise’s Board of Directors before submission to FHFA for review. The directive takes effect immediately and calls for implementation “as soon as reasonably practical.”

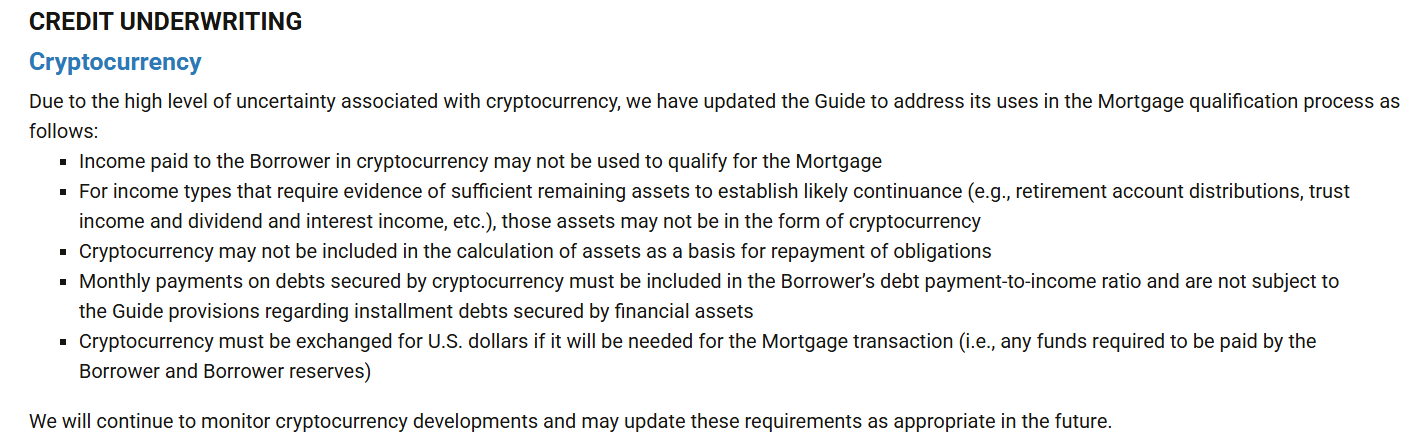

Crypto assets are generally not accepted as mortgage reserves unless converted into US dollars. In 2021 guidance, Freddie Mac explicitly stated that crypto may not be included in the calculation of assets as a basis for mortgage repayment and must be exchanged for US dollars for mortgage transactions.

Likewise, lenders are typically required to convert crypto assets into cash or cash equivalents before counting them as reserves, due to volatility and regulatory uncertainty.

If approved, the move could help integrate crypto assets more fully into traditional mortgage finance, making borrowing more accessible to crypto holders.

Share this article